Student loan debt is not just a financial issue; it is a mental health issue, a workforce issue, and a generational equity issue.

According to data from EdTrust, more than 43 million Americans carry student loan debt, but the burden is far from evenly shared. Black women, in particular, hold the highest average student loan debt of any demographic group, often borrowing more to pursue education while earning less once they graduate. Years after completing college, Black women still owe significantly more than their peers, not because of poor financial choices, but because of systemic inequities in wages, wealth, and burdensome repayment options.

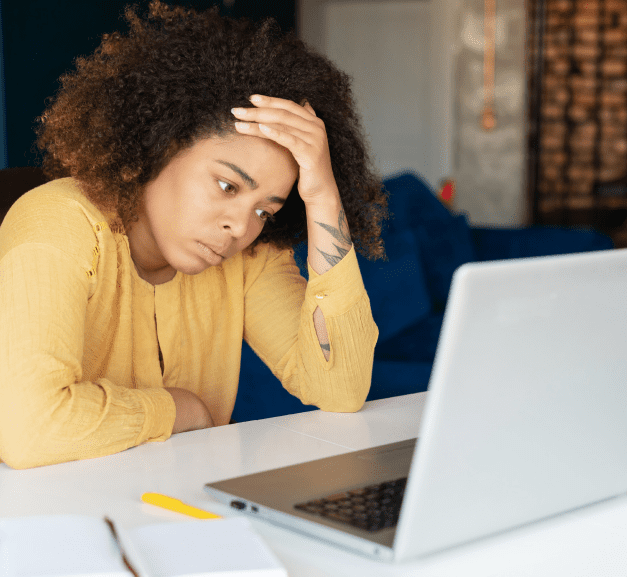

This debt doesn’t just live on paper. Research consistently links student loan debt to higher levels of stress, anxiety, and depression, as well as delayed life milestones such as homeownership, starting a family, and saving for retirement. For borrowers already struggling to make ends meet, the return of aggressive collection practices can deepen feelings of panic, shame, and exhaustion.

Be clear about this truth: student loan debt is a policy failure, not a personal one. Borrowers, especially Black women, have shouldered higher costs, earned lower wages, and received fewer protections, all while being told to simply manage better. The strain you feel is not a reflection of your choices, but of a system that has normalized inequity and called it responsibility.

As the Trump administration resumes collection efforts, including wage garnishment, many borrowers are confronting not only shrinking paychecks but also the emotional weight of a system that offers little margin for error. For Black women and other traditionally underserved borrowers, this moment is especially heavy, as they continue to carry debt while supporting families, communities, and workplaces.

If this is you, know this: you are not failing. You are navigating a broken system, and you are not alone.

After the COVID-19 pandemic repayment pause, student loan borrowers were given a temporary reprieve from monthly payments. Now, as wage garnishment and other collection efforts ramp up, many are left wondering how to absorb this renewed financial strain and reintegrate payments into already tight budgets.

As a former financial advisor, I’m all too familiar with the weight of student loans and the stress they place on people at every age and income level. With wage garnishment already underway, borrowers in default may feel the impact immediately in their paychecks, often without warning.

Today, as a money strategist who focuses on addressing the core of people’s financial challenges, my work centers on helping individuals regain a sense of control. If your student loans are in default, wage garnishment is a real possibility, but it does not have to define your future. Clarity, awareness, and strategy can help you move forward, even if you are already playing catch-up.

If you are struggling to make the math work, pause here. Many borrowers are already underemployed, juggling multiple jobs, or working below their skill level, while the cost of housing, food, child care, and transportation continues to rise. For people already doing everything they can, the return of wage garnishment is not just stressful; it is predictably cruel.

In this moment, the goal is not to work harder or hustle more. It is to reduce harm, protect your income, and stabilize your household as much as possible. So, what should you do:

- Start with clarity, not panic. Understanding exactly where your loans stand is one of the few levers borrowers still have. Contact your loan servicer to confirm your loan status and ask what options exist to pause or limit collection activity. If you know your loans are in default, contact the Default Resolution Group. The most common ways to get out of default are loan rehabilitation and consolidation. There are also nonrepayment options, such as Total and Permanent Disability Discharge, which are more difficult to obtain. If you are delinquent, contact your loan servicer to learn about more affordable repayment options or ways to pause your payments.

- Even when options seem limited, having accurate information can restore a sense of agency.

- Focus on stabilization, not perfection. If your loans are in default, it may feel impossible to fit another bill into an already strained budget. This is not a failure of discipline; it is the reality of an economy that has made survival more expensive. Protect essentials like housing, food, healthcare, and child care first. Financial stability begins with security.

- Buy time where you can. Time is often more valuable than money during periods of financial strain. This may mean seeking temporary flexibility from other creditors, pausing nonessential payments, or exploring employer-based benefits such as hardship programs, employee assistance programs (EAPs), or payroll accommodations. Buying time can prevent more serious financial damage while you assess longer-term options.

- Do not assume you must do this alone. Nonprofit credit counselors, legal aid organizations, and worker advocacy groups can help borrowers understand wage garnishment protections and their rights. Seeking support is not a sign of weakness; it is a necessary response to a system that places undue pressure on individuals.

For borrowers already exhausted by side hustles and caregiving, survival itself is a strategy. Reducing harm, preserving stability, and protecting your mental health are legitimate financial goals.

And even with planning, it’s important to say this plainly: student loan debt is a national financial crisis. It is not a personal failure, and it is not a burden you should carry alone. These are not normal circumstances, but that does not mean you cannot survive them. Let this be your reminder: this debt does not define you. You did what society told you would lead to opportunity and stability, and you are now navigating the consequences of a system that did not uphold its end of the bargain.

Be clear about this truth: student loan debt is a policy failure, not a personal one. Borrowers, especially Black women, have shouldered higher costs, earned lower wages, and received fewer protections, all while being told to simply manage better. The strain you feel is not a reflection of your choices, but of a system that has normalized inequity and called it responsibility.

So, take the steps you can. Make the call. Build the plan. Adjust the budget. Do not internalize a burden that was never meant to be yours. Progress may feel slow, but every action you take is moving you in the right direction.

This moment is heavy, but it is not permanent. You are not behind. You are not broken. You are navigating an unjust system with resilience and resolve.

And one day, this chapter will read not as the moment you were overwhelmed, but as the moment you refused to give up.

Shavon Roman is the founder and chief money strategist at Heal. Plan. Invest.

As part of our commitment to elevating diverse perspectives, EdTrust occasionally features guest blogs. The views expressed are those of the author and do not necessarily reflect EdTrust’s views or positions.

January 14, 2026 by Shavon Roman, Chief Money Strategist

January 14, 2026 by Shavon Roman, Chief Money Strategist