EdTrust in Texas advocates for an equitable education for Black and Latino students and students from low-income backgrounds across the state. We believe in centering the voices of Texas students and families as we work alongside them for the better future they deserve.

Midwest

Our mission is to close the gaps in opportunity and achievement that disproportionately impact students who are the most underserved, with a particular focus on Black and Latino/a students and students from low-income backgrounds.

New York

EdTrust–New York is a statewide education policy and advocacy organization focused first and foremost on doing right by New York’s children. Although many organizations speak up for the adults employed by schools and colleges, we advocate for students, especially those whose needs and potential are often overlooked.

Tennessee

EdTrust-Tennessee advocates for equitable education for historically-underserved students across the state. We believe in centering the voices of Tennessee students and families as we work alongside them for the future they deserve.

West

EdTrust–West is committed to dismantling the racial and economic barriers embedded in the California education system. Through our research and advocacy, EdTrust-West engages diverse communities dedicated to education equity and justice and increases political and public will to build an education system where students of color and multilingual learners, especially those experiencing poverty, will thrive.

Louisiana

The Education Trust in Louisiana works to promote educational equity for historically underserved students in the Louisiana’s schools. We work alongside students, families, and communities to build urgency and collective will for educational equity and justice.

Texas

EdTrust in Texas advocates for an equitable education for historically-underserved students across the state. We believe in centering the voices of Texas students and families as we work alongside them for the better future they deserve.

Massachusetts

The Education Trust team in Massachusetts convenes and supports the Massachusetts Education Equity Partnership (MEEP), a collective effort of more than 20 social justice, civil rights and education organizations from across the Commonwealth working together to promote educational equity for historically underserved students in our state’s schools.

Home – EdTrust Comment on the Department of Education’s Proposed Rule Regarding Student Debt Cancellation

EdTrust Comment on the Department of Education’s Proposed Rule Regarding Student Debt Cancellation

We commend the Department for its continued commitment to providing student debt relief to the millions of borrowers who are harmed by student debt.

May 17, 2024 by EdTrust

Richard Blasen Office of Postsecondary Education U.S. Department of Education 400 Maryland Ave., SW Washington, DC 20202

RE: Student Debt Relief for the William D. Ford Federal Direct Loan Program (Direct Loans), the Federal Family Education Loan (FFEL) Program, the Federal Perkins Loan (Perkins) Program, and the Health Education Assistance Loan (HEAL) Program (Docket ID ED-2023-OPE-0123)

On behalf of EdTrust, an organization committed to advancing policies and practices to dismantle the racial and economic barriers embedded in the American education system, thank you for the opportunity to comment on the U.S. Department of Education’s (“the Department”) request for comment on the proposal to amend the regulations related to the Higher Education Act of 1965 (HEA), as amended to provide for the waiver of certain student loan debts.

We commend the Department for its continued commitment to providing student debt relief to the millions of borrowers who are harmed by student debt. After a pandemic,[1] record high inflation,[2] increasingly unaffordable housing,[3] and wages that have failed to keep pace with rising costs for decades,[4] student debt is a financial burden that many Americans can no longer afford to bear. Millions of borrowers were denied up to $20,000 in student debt relief after the U.S. Supreme Court struck down the Biden administration’s original student debt relief plan.[5] The 43 million Americans with federal student debt are counting on the Department to fulfill President Biden’s promise to provide broad-based student debt relief.[6]

We applaud the Department for proposing to waive repayment of the following amounts:

The outstanding balance of a loan for borrowers who would be otherwise eligible for forgiveness under an IDR plan or an alternative repayment plan but who are not currently enrolled in such a plan

The outstanding balance of a loan for borrowers determined to be otherwise eligible for loan discharge, cancellation, or forgiveness, but who did not successfully apply

The outstanding balance of a loan obtained to pay the cost of attending an institution or program where the Secretary or other authorized Department official has issued a final decision, denial of recertification, or determination that terminates or otherwise ends the institution’s or program’s title IV eligibility due at least in part to the institution’s or program’s failure to meet required accountability standards based on student outcomes or to its failure to provide sufficient financial value to students

The outstanding balance of a loan obtained to pay the cost of attending an institution or program that closed and the Secretary or other Department official has determined the institution or program failed, for at least one year, to meet an accountability standard based on student outcomes, or failed to deliver sufficient financial value to students and there was a pending program review, investigation, or other Department action at the time of closure

The outstanding balance of a loan that is associated with enrollment in a Gainful Employment (GE) program that has closed and prior to closure had high debt-to-earnings rates or low median earnings rates

In the case of FFEL Program loans held by a private loan holder or a guaranty agency, the outstanding balance of a FFEL Program loan when a loan first entered into repayment on or before July 1, 2000; when the borrower is otherwise eligible for, but has not successfully applied for, a closed school discharge; or when the borrower attended an institution that lost its title IV eligibility due to a high cohort default rate (CDR), if the borrower was included in the cohort whose debt was used to calculate the CDR or rates that were the basis for the institution’s loss of eligibility[7]

We applaud the Department for recognizing how damaging — financially and psychologically — runaway interest and interest capitalization can be for borrowers.[8] However, the magnitude of the student debt crisis requires a bolder approach. The Department has proposed waiving the full amount, by which the current outstanding balance on a loan exceeds the amount owed when the loan entered repayment for loans being repaid on any Income-Driven Repayment (IDR) plan if the borrower’s income is at or below $120,000 if the borrower’s filing status is single or married filing separately; $180,000 if a borrower files as head of household; or $240,000 if the borrower is married and files a joint federal tax return or the borrower files as a qualifying surviving spouse. For borrowers not using IDR, the Department has proposed waiving up to $20,000 of the current balance that exceeds the original balance when a borrower entered repayment.[9] This proposed form of relief is helpful for borrowers who have been in repayment for years or decades and owe more than they originally borrowed. However, while we appreciate this proposal, the income caps for borrowers using IDR and the $20,000 cap on relief for all other borrowers limit how beneficial this relief could be for borrowers, especially Black borrowers, who have fewer resources to repay their loans due to wage and wealth gaps.[10] We encourage the Department to eliminate income caps for borrowers who are enrolled in IDR and lift the $20,000 cap on relief for all other borrowers.

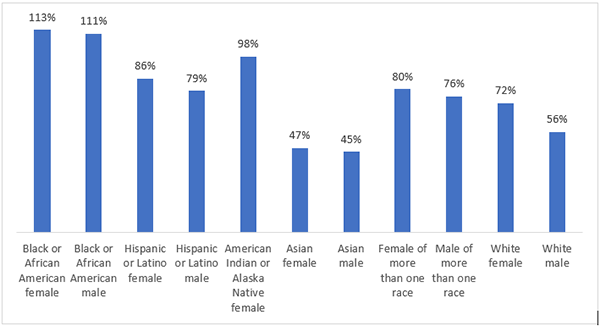

In 2020, EdTrust, in partnership with Dr. Jalil Bishop, conducted the National Black Student Debt Study. The study included 1,300 survey responses and 100 in-depth interviews with Black borrowers.[11] One of the four main findings was IDR plans felt like a lifetime debt sentence.[12] Borrowers felt this way because of the runaway interest and ballooning balances that can occur when borrowers use an IDR plan. Black borrowers have the worst repayment outcomes and the most balance growth due to interest. Twelve years after starting college, Black women and Black men owe 13% and 11% more than they borrowed respectively, which is more than any other racial and ethnic group (Figure 1).[13]

FIGURE 1: Ratio of amount owed to amount borrowed for federal loans 12 years after starting college

Source: EdTrust analysis of U.S. Department of Education, National Center for Education Statistics, Beginning Postsecondary Students: 2004/2009 (BPS).

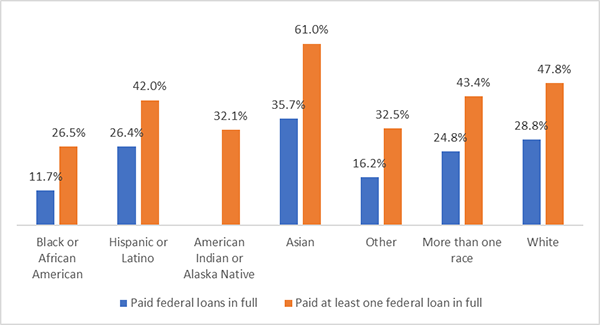

We appreciate the Department’s proposal to waive a borrower’s outstanding balance for loans borrowed for undergraduate education if they entered repayment on or before July 1, 2005, and to waive a borrower’s outstanding balance if they entered repayment on or before July 1, 2000, if they have any loans for graduate study. However, we hope the Department will consider implementing the 20- and 25-year debt relief on a rolling basis for borrowers who entered repayment after July 1, 2005, or July 1, 2000. Systemic issues and abuses in loan servicing, which extended and continue to extend borrowers repayment timeline beyond 20 or 25 years, prompted the administration to create the IDR account adjustment.[14] Providing debt relief on a rolling basis would be helpful for all borrowers, especially Black borrowers, who take the longest to repay their debt (Figure 2).

Figure 2: Percentage of borrowers (by race/ethnicity) who started college in 2004 and had repaid all federal student loan debt or at least one federal student loan (or any federal student loan) within 12 years

Source: U.S. Department of Education, National Center for Education Statistics, Beginning Postsecondary Students: 2004/2009 (BPS).

Note: “Paid federal loans in full” for American Indian or Alaska Native borrowers is not included because reporting standards were not met.

Of the Black borrowers who began their postsecondary education in 2004, only 11.7% had fully repaid their federal student debt 12 years later — i.e., by June 30, 2015 (Figure 2).[15] Just 3.3% had fully repaid their loans without defaulting or having a portion of their loan discharged.[16]

Student debt relief is a racial justice issue. Expanding access to relief is important for helping Black borrowers and other borrowers who are excluded from the current relief proposal.

We thank the Department for taking action to provide debt relief to borrowers, and we ask that the Department consider incorporating our recommendations into the final debt relief plan.

We are happy to respond to any questions you may have about this letter’s contents; please contact Victoria Jackson, assistant director of Higher Education Policy, or Reid Setzer, director of Government Affairs. Thank you for your consideration.

[3] Jennifer Ludden, “Housing Is Now Unaffordable for a Record Half of All U.S. Renters, Study Finds,” NPR, January 25, 2024, sec. National, https://www.npr.org/2024/01/25/1225957874/housing-unaffordable-for-record-half-all-u-s-renters-study-finds. https://www.npr.org/2024/01/25/1225957874/housing-unaffordable-for-record-half-all-u-s-renters-study-findshttps://www.npr.org/2024/01/25/1225957874/housing-unaffordable-for-record-half-all-u-s-renters-study-finds

William Darity Jr., Darrick Hamilton, Mark Paul, Alan Aja, Anne Price, Antonio Moore, and Caterina Chiopris, What We Get Wrong About Closing The Racial Wealth Gap (Samuel DuBois Cook Center on Social Equity and Insight Center for Community Economic Development, April 2018), https://socialequity.duke.edu/wp-content/uploads/2020/01/whatwe-get-wrong.pdf

May 17, 2024 by EdTrust

May 17, 2024 by EdTrust