The One Big Beautiful Bill Act (OBBBA) included sweeping changes to higher education, but now that its provisions are becoming reality, one is drawing growing concern: new limits on federal graduate loans. What may have seemed technical on paper could have profound consequences, pricing low-income students and students of color out of advanced degrees or pushing them into costly private debt, further widening gaps in who gets to pursue graduate education.

Eliminating the Grad PLUS loan program would not reduce the need for student borrowing unless the cost of attendance declines, and it would significantly withdraw federal investments from states, reduce access to advanced degrees, strain institutional finances, and disrupt workforce pipelines in sectors already facing shortages.

Since July 1, 2006, the Grad PLUS loan program has allowed graduate students to borrow up to the full cost of attendance. As of July 1, 2026, that will no longer be the case. The policy changes made through the One Big Beautiful Bill Act (OBBBA) will eliminate Grad PLUS loans completely and cap graduate borrowing on both an annual and an aggregate basis. Under the new federal loan limits, borrowing for graduate programs — all master’s and Ph.D. programs not included in the “professional” definition — will be capped at $20,500 per year with a lifetime limit of $100,000. Professional doctoral programs, such as medicine and law, will have a higher borrowing limit capped at $50,000 annually and $200,000 in total.

Grad PLUS loans have been a vital part of federal student aid for graduate students, accounting for billions in annual federal loan disbursements and helping hundreds of thousands of students access graduate-level education. The elimination of these loans was not accompanied by new investments in grant aid or other affordability-focused initiatives that could reduce reliance on borrowing. Additionally, the legislation does not include provisions that require or incentivize states and institutions to lower costs or expand financial support for graduate and professional students, leaving a critical gap in college affordability.

At the same time, concurrent changes to student loan repayment structures, such as updates to Public Service Loan Forgiveness (PSLF), may reshape borrowers’ long-term repayment trajectories and access to loan forgiveness.

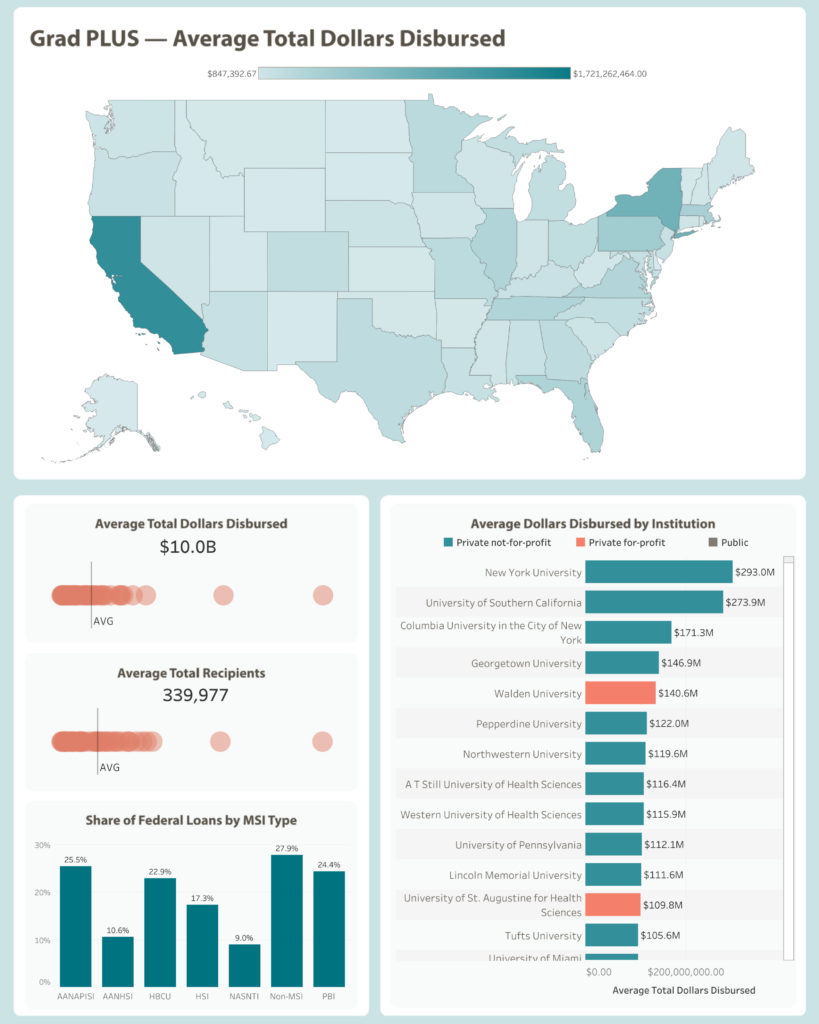

In recent years, roughly 440,000 students borrowed through the Grad PLUS loan program, amounting to over $14 billion annually. As a result, these new loan limits will have widespread effects not only on students but also on states and their labor markets. Graduate and professional education is an engine of opportunity not just for individuals but also for the entire state’s economy.

In a report by Georgetown University McCourt School of Public Policy, researchers found that by 2031, an estimated 17% of all jobs nationwide will require a graduate degree. At the same time, data from the Bureau of Labor Statistics show that more than 100 occupations already typically require a graduate degree for entry, underscoring how essential these credentials are for accessing a wide range of careers. These policy changes will likely limit access to graduate education, leaving many Americans without a sustainable pathway to a graduate degree.

Why These Changes Matter

With the elimination of the Grad PLUS loan program and new federal borrowing caps, many students will likely face a gap between the total cost of graduate education and what they can borrow through federal loans. For students in ‘non-professional’ graduate programs, that gap is especially stark, with typical student budgets exceeding the $20,500 annual loan cap by more than $8,000 per year. Without access to the Grad PLUS loan program, borrowing limits could restrict access to graduate school, especially for women and students of color who are already more likely to rely on federal loans. But private loans are not a reliable backstop. A recent report found that over 40% of Americans would likely be denied access to private student loans due to credit and income requirements, with even higher exclusion rates for Pell Grant recipients and borrowers of color.

What the Dashboard Shows

The Graduate Borrowing Landscape dashboard offers interactive tools that let users explore how Grad Plus borrowing varies by state and institution, including total funding levels and borrower reliance across regions. The dashboard also shows how dependent many students are on Grad PLUS loans to finance their education.

May 05, 2026 by Tihirah Ruffin, Noppakan Sirikul, Tionna Ellis, Brianna Huynh

May 05, 2026 by Tihirah Ruffin, Noppakan Sirikul, Tionna Ellis, Brianna Huynh