The ‘Black Tax’ Is Key to Understanding and Solving the Black Student Debt Crisis in the Time of COVID-19 and Beyond

It’s no secret that Black people must work harder and pay more to receive the same benefits and opportunity as their White or non-Black peers. This phenomenon is commonly known as the “Black tax.” Unfortunately, it’s becoming clear that the COVID-19 crisis is increasing the cost of being Black in America even more.

The Cut reports that Black Americans Are Disproportionately Dying of Coronavirus. Meanwhile, Black residents in states like Illinois, Michigan, North Carolina, and Louisiana are far more likely to test positive for COVID-19 than White residents in these states, according to an article in ProPublica. That’s devastating, but not surprising news. COVID-19 does not discriminate, but people do. If you’re Black in America, you’re less likely to have health insurance and more likely to have conditions like diabetes and hypertension, which increase the risk of contracting and dying from COVID-19. If you’re Black, you’re also more likely to have a low-paying job that requires social contact, and you’re less likely to be able to work from home or have savings that would allow you to stock up on basic supplies and withstand the financial strain of unemployment.

As Congress considers what to do next to address this deepening public health and economic disaster, it must account for the disproportionate cost of being Black in America. That will mean tackling the Black student debt crisis that was spiraling out of control well before the new coronavirus showed up.

The research suggests that, despite the challenges of student debt and low graduation rates, going to college still pays off, on average, with college graduates having better social and economic outcomes than their peers. But there’s a reason it’s said that “when America gets a cold, Black people get pneumonia” (or now, even worse, COVID-19):

For Black people living at the margins, the ugly truth is that no matter the crisis, the highest cost will always be borne by them. The student debt crisis is no exception.

Black students are more likely to borrow, borrow more, struggle with repayment, and default on their student loans than their peers. Data on student debt default rates illustrates the uniqueness and severity of the crisis for Black borrowers. Default occurs after a borrower is 270 days late and is the most disastrous financial outcome of student debt. Defaulting not only ruins a person’s credit, but it makes future borrowing more expensive and can make it harder to get a job, rent an apartment, or buy a house or a car. Half of Black borrowers who entered college in the 2003-04 academic year defaulted on their student loans within 12 years. What’s more, protective factors like degree completion or high family income, which would normally shield borrowers from adverse debt outcomes, don’t necessarily protect Black borrowers. In fact, a Black bachelor’s degree recipient is more likely to default than a White college dropout, and Black borrowers from families in the highest income quintile have higher default rates than White borrowers in the lowest income quintile (see Table 1).

| Family Income | Black Default Rates | White Default Rates | Black AGI | White AGI |

|---|---|---|---|---|

| Low | 48% | 23% | $ 14,250 | $ 15,761 |

| Lower middle | 40% | 15% | $ 41,920 | $ 41,940 |

| Upper middle | 36% | 9% | $ 69,228 | $ 70,449 |

| High | 34% | 5% | $ 129,291 | $ 132,348 |

| Overall | 42% | 11% | $ 38,168 | $ 71,367 |

Note: Family Income: Low < $32,000, Low middle ≥ $32,000 & < $60,000, High middle ≥ $60,000 & < $92,000, High ≥ $92,000

Source: Ed Trust analysis of U.S. Department of Education, National Center for Education Statistics, 2003-04 Beginning Postsecondary Students Longitudinal Study, Second Follow-up (BPS:04/09).

But let’s be clear. The student debt issue has reached crisis level in part because it impacts more than one-third of Black people that go on to college or the 30% of Black adults with an associates’ degree or higher, but because it impacts Black people more broadly. For example, there are great risks and costs for those who avoid postsecondary education out of a fear of debt, as people without any college credits or a degree face greater social and economic challenges. Additionally, those with debt have a more limited ability to invest in their families and communities. And according to an analysis by economists at the New York Fed, student loan balances are greater and rising faster in majority-Black neighborhoods than in majority-White ones. Default rates are higher in Black neighborhoods, too. This has far-reaching consequences, leaving many Black people with a lower net worth, and less money left over for long-term savings, a down payment on a house, not to mention fewer resources to invest in local schools, businesses, and communities.

Factors and policies beyond higher education are largely to blame. Thanks to de jure housing segregation in the 20th century and de facto housing segregation today, coupled with the inequitable and often unconstitutional funding of public K-12 education, too many Black students are concentrated in under-resourced K-12 schools that are unable to offer them the preparation that colleges require. As a result, many Black students are segregated in less-selective colleges. Meanwhile, thanks to rampant employment discrimination and the racial wage gap, Black people tend to be concentrated in low-paying jobs, too. It’s no wonder the typical Black household has an income of $35,400 compared to $61,200 for a typical White household. But the cumulative effects of racist policy and practice don’t end there.

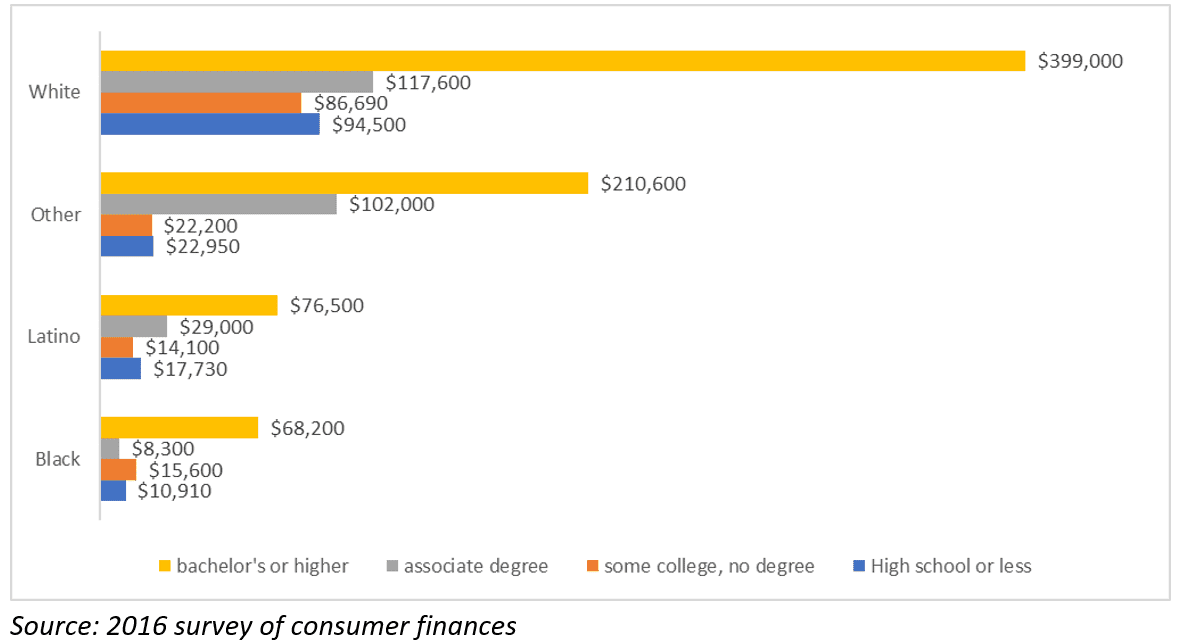

Despite the economic strides many Black families have made since the civil rights era of the 1960s, the long legacy of slavery, Jim Crow, and racist federal housing policy, combined with ongoing discrimination in employment and lending, have effectively prevented many Black families from building wealth through homeownership, leaving them with a fraction of the wealth of White people. The net worth of a typical Black household in 2016 was only $17,600 compared to $171,000 for a White household. This discrepancy is compounded by poor higher education policy, which has made a college education virtually unaffordable for students from low-income backgrounds and students of color — particularly Black students, who have fewer family resources to help pay for college or repay debt (see Table 2). Unfortunately, a higher education does not close the racial wealth gap. The typical Black household headed by an individual with a bachelor’s degree or higher has a lower net worth than a typical White household headed by an individual with a high school education or less (see Figure 1).

States spend less on institutions that serve greater shares of Black students.

As a result of deliberate policy choices, states fund less-selective community colleges and public four-year colleges at significantly lower rates per student than selective public colleges. Over time, this gap as widened. Since a disproportionate share of Black students attend less-selective institutions, this effectively means that states spend far less on Black students than on their White peers — about $1,000 less per student, in fact. Yet, this alone does not fully explain the stratification within the system.

State governments operate racially segregated and unequal systems of higher education.

But don’t take our word for it. Several court verdicts have concluded that some states are systematically shortchanging colleges serving greater shares of Black students. And since Black students are underrepresented even at public colleges and community colleges, Black students’ opportunity to access and complete college is severely limited.

Black students are harmed the most by state cuts to higher education.

For several decades, states cut higher education funding, as public colleges hiked tuition, leaving students and their families to shoulder more of the costs. After the Great Recession, most states slashed higher education funding even further — so much so, that now, more than 10 years later, funding has still not recovered. On average, states spent $1,220, or 13% less per student in 2018 than in 2008, after adjusting for inflation. Meanwhile, state budget cuts to higher education have been particularly hard on Black students, who, as noted earlier, generally have less family wealth to fall back on. Research by the Center on Budget and Policy Priorities shows that while the average net price for a public four-year university comprised 23% of the national median household income in 2017, it took up a whopping 40% or more of the median household income for Latino and Black families in seven and 17 states, respectively.

The nation’s higher-education policy isn’t helping matters either. The Pell Grant is the largest federal need-based aid program, and Black students have the highest rate of participation in the program, at 58% versus 32% for White students. Unfortunately, as Black enrollment in higher education has inched up over the decades, the purchasing power of the Pell Grant has sharply declined. In 1975, the Pell Grant covered 79% of the cost of attending a public university. Today, Pell Grants only cover 28%. Many Black students and their families have had to take on loans to make up the difference.

Meanwhile, the federal government’s failure to protect students from predatory for-profit institutions is making matters worse. This lack of oversight disproportionately harms Black students because they are overrepresented at for-profit institutions. Three in four Black student borrowers who attended a for-profit college and did not complete their degree defaulted on their loans.

Last year, Sens. Catherine Cortez Masto (D-N.M.), Kamala Harris (D-Calif.), Doug Jones (D-Ala.), and Elizabeth Warren (D-Mass.) led an effort to confront the student debt crisis for borrowers of color and asked higher-education experts for solutions. In the past, The Education Trust might have simply offered recommendations on ways to protect students from predatory and fraudulent colleges, improve college graduation rates, and increase need-based financial aid, so students from low-income backgrounds do not have to borrow in the first place. But we must recognize that race-neutral approaches are not enough to solve the Black student debt crisis. The data contradicts the old adage that “a rising tide lifts all boats.” Black students who graduate from non-predatory colleges still struggle, and the likelihood of increasing need-based aid like Pell Grants to the point that loans become unnecessary is slim, given that Democrats and Republicans proposed increasing the grants by just $500 and $20, respectively, in 2019. Lastly, existing student debt policies, like income-driven repayment have not made a difference for Black borrowers either. The evidence is clear, the Black student debt crisis is a racial justice problem that requires racial justice solutions.

The Education Trust, in partnership with several Black scholars, embarked on this essay series to analyze why Black borrowers struggle so much with student debt and to offer actionable policy solutions.

Big problems call for big solutions, and the best solutions tend to come from the people who understand the problem and have been impacted by it firsthand. Far too often, though, Black people are left out of discussions about the Black student debt crisis. This series aims to change that.

We invited higher-education experts from the Black academic community to share their bold ideas, plans and solutions to the Black student debt crisis. Their essays cover the following topics: the racial wealth gap; racial capitalism – a term used by Cedric Robinson, a University of Denver law professor, to explain modern capitalism’s dependence on slavery, violence, imperialism, and genocide – and the need to improve job quality; the need for better borrower protections and regulation of for-profit colleges; the need for more investment in institutions that serve the greatest share of Black students, like Historically Black Colleges and Universities (HBCUs) and Predominately Black Institutions; and the need for large-scale college affordability policy and reparations. The authors move beyond the startling statistics to offer solutions tailored to Black borrowers. This series also highlights the need for greater funding and need-based aid and more targeted investment. While there may be no single quick fix to the complicated Black student debt crisis, the recommendations put forth here are an important first step in addressing it.

Every idea presented in this series deserved careful consideration before the new coronavirus threatened the lives and livelihoods of all Americans – Black Americans especially. But now, in the midst of this deadly pandemic, proposals like these, which account for the disproportionate cost of being Black in America, are more important than ever. Any response put forth to help people at this time should operate from the assumption that, though the virus is widespread, its impact will be disproportionately felt by certain segments of the population because of pre-existing inequities. In the coming weeks, for example, Congress could take up the issue of canceling student debt. If so, it might take the bold step to forgive $10,000 of debt for every borrower, as one author has suggested, or up to $50,000 in targeted forgiveness, as Sen. Warren has proposed. Considering that the average loan total of Black bachelor’s degree holders is more than $30,000, a sensible middle road might be to cancel at least $20,000 of student debt for those earning less than $100,000 per year, scaled down for those earning up to $200,000 per year. The important thing is that our public officials take seriously the clear evidence of a Black tax in America and tailor policy solutions to compensate for it. The current crisis has made it abundantly clear that what impacts one individual or family impacts everyone. It is our hope that this recognition may inspire support for targeted solutions that could have collective benefits during the COVID-19 crisis and beyond.

Victoria Jackson is a senior policy analyst at The Education Trust.

Tiffany Jones is senior director of higher education policy at The Education Trust.

January 14, 2026 by Shavon Roman, Chief Money Strategist

January 14, 2026 by Shavon Roman, Chief Money Strategist Student loan debt isn’t just a financial issue; it affects mental health, workforce, and generational equity. Here’s what you need to know about wage garnishment

September 17, 2025 by Roxanne Garza

September 17, 2025 by Roxanne Garza During a shadow hearing, students and borrowers, most of whom were the first in their family to attend college, testified about their worries of how they would pay off their student loans

June 04, 2025 by Gabriela Montell

June 04, 2025 by Gabriela Montell A student at a private university in Colorado describes her academic journey and how this administration’s policies are impacting students and campus life at her college